Adults in the United States have a number that virtually dictates their finances. The number is your credit score. Using credit scores as a part of processing your mortgage application started in 1995; now all financial institutions rely on it heavily to evaluate an applicant’s credit-worthiness.

Your Credit Score

Your credit score is a calculation that is based on information contained in your credit report. This resulting number allows lenders to objectively and quickly determine, if you are a good credit risk, and if you are diligent about repaying your loans. Scores range from 300 to 900, but most people fall between 500 and 700. The higher the score, the better risk lenders will consider you.

The score itself is relative and will be viewed differently by creditors depending on numerous factors, including the creditor’s risk level, marketing goals and business practices. Your risk score will change over time as your credit history develops.

The guru of the credit-scoring world is Fair, Issac and Company, also known as FICO. They have created the most common credit scoring model that is used by the Big 3 credit companies: Equifax, Experian and TransUnion. Sophisticated mathematical processes calculate the score by assigning numerical values to various pieces of information in the credit report.

What makes up my credit score?

There are five categories that make up your overall score:

- Payment History (35%) – Have you paid your bills on time? This rates heavily. Bankruptcies and foreclosures are also considered here.

- Amounts Owed (30%) – How much do you owe and how many accounts do you have open? Rising balances, maxed out credit cards, new credit requests and high balances on installment loans are red flags.

- Length of Credit History (15%) – How long have you had established credit? Starting young and paying off your balances is a bonus.

- Types of Credit in Use (10%) – What’s your “credit mix?” Using a lot of finance companies with higher interest rates is a negative; so are people with no credit in use, since there is a question of whether one can manage credit responsibly.

- New Credit (10%) – Have you done a lot of “credit stuff” recently? Multiple checks on your credit from companies will lower your score. Tip: If you’re shopping around for the best refinancing rates, do it fast and furious. FICO will not penalize you if there’s a short period of time that your credit is being checked. For example, mortgage inquiries made in any 14-day period will count as one inquiry.

How do I obtain my credit score/report?

The first thing you need to do before shopping for a mortgage is review your credit reports for errors. Because if you have incorrect or outdated information that’s lowering your score-and, therefore, raising the interest rate you’ll have to pay-it can be removed, but it takes at least 60 to 90 days.

There are three national credit-reporting agencies, Equifax, Experian and TransUnion. Your credit report (not the score) from these agencies is free thanks to the Federal Trade Commission that ruled every American is entitled to a free credit report from each agency every 12 months. The free report will be mailed to you and could take 15 days. If you wish to have a report from each of the three credit companies you have to request them individually.

For the most detailed explanations on your FICO scores, go to the credit education area at www.myfico.com. For about $40 you can purchase all three reports with credit scores. It’s useful to buy all three because large lenders either average the scores or take the middle one. You’ll want to check your FICO scores once a year or several months before you apply for a loan.

As a general rule, a negative report stays on the record for seven years, a bankruptcy for 10 years. The Federal Trade Commission’s web site presents a concise summary of your rights, written in language that’s easy to understand.

Credit Bureaus and Your Financial Information

A credit bureau or credit reporting agency is in the business of gathering, maintaining and selling information about consumers’ credit histories. It collects information about consumers’ payment habits from credit grantors like banks, savings and loans, credit unions, finance companies and retailers. The credit bureau stores this information in a computer database and sells it to credit grantors in the form of credit reports.

When you apply for mortgage refinancing the lender or broker orders your credit report from at least one credit bureau and analyzes the information to decide whether to grant you credit. The credit bureau charges the lender a fee for every credit report sold.

Although credit-reporting agencies provide your credit report to lenders when you apply for credit, they do not make actual lending decisions. It is up to individual lenders to evaluate your credit report along with other factors they consider important and then decide whether or not to offer you credit.

A consumer credit report is a document that contains a factual record of an individual’s credit payment history. Mortgage refinancing lenders are permitted by law to review your credit report to objectively determine whether to grant you credit. There are 190 million credit active people in the United States who have a charge account, car loan, student loan or home mortgage. As those people pay their bills, most lenders report credit payment information to credit bureaus. So most of the information in your consumer credit report comes directly from the companies you do business with.

A consumer credit report contains four types of information: identifying information, credit information, public record information and inquiries.

- Identifying information includes:

• Your name

• Your current and previous addresses

• Your Social Security number

• Your year of birth

• Your current and previous employers

• If you’re married, your spouse’s name - Credit information includes credit accounts or loans you have with:

• Banks

• Retailers

• Credit card issuers

• Other lenders - Public record information includes any information that’s contained in state and county court records, like:

• Bankruptcies

• Tax liens

• Monetary judgments - Inquiries indicate to other credit grantors that you have applied for new credit that could result in additional debt. Potential lenders view multiple recent inquiries on your credit report as a sign that you are overextending yourself.

(A credit risk score may also be included when your report is provided to a credit grantor, although it is not included on consumer review reports. The ways to calculate and use a credit score vary widely, so a score has little meaning outside of the context of a particular lender’s unique guidelines for use. Therefore, it is not included on consumer review reports.)

Your consumer credit report does not contain information about your race, religious preference, medical history, personal lifestyle, personal background, political preference or criminal record.

Positive credit information remains on your report indefinitely, although information about an account will cycle off your report if no new information is reported about it for seven years. (Thus, a closed account will disappear from your report seven years after it is reported closed by the credit grantor.)

Most negative information remains for up to seven years. Bankruptcies can remain on your credit report for up to ten years. Other public record information can remain for up to seven years.

Most inquiries stay on your credit report for up to two years.

Mortgage report

A mortgage report is a special credit report that lenders use prior to deciding whether or not to extend you a home loan. Each report is compiled from credit reports from two or three credit bureaus. The mortgage credit reporting company purchases credit reports from the credit bureaus, combines them and manually verifies specific information such as employment, credit account balances and public record information.

Federal law carefully regulates how credit reports can be used and by whom. By law, you have the right to obtain your own reports at a reasonable price. Businesses must offer proof, before they can access consumer credit information, that they will be using the data for no other purpose than that allowed by federal law.

What the Credit Numbers Mean when Refinancing

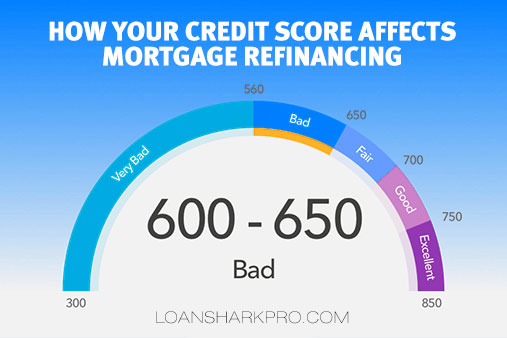

Credit scores range from 375 to 900 points, but those numbers mean little on their own. They become meaningful and useful within the context of a particular lender’s own cutoff points and underwriting guidelines.

In general, you are likely to be considered a better credit risk if your FICO score is high. Under mortgage lending guidelines, for example, a score of 650 or above indicates a very good credit history. People with these scores will usually find obtaining credit quick and easy, and will have a good chance to get it on favorable terms.

Scores between 620 and 650 (average FICO scores fall into this range) indicate basically good credit, but also suggest to lenders that they should look at the potential borrower to assess any particular credit risks before extending a large loan or high credit limit. People with scores in this range have a good chance at obtaining credit at a good rate, but may have to provide additional documentation and explanations to the lender before a large loan is approved. This means that their loan closing may take longer, making their experience more like that of borrowers in the days before credit scoring, when every individual was researched.

A score below 620 may prevent a borrower from getting the best interest rates, as they may be considered a greater credit risk-but it does not mean that they can’t get credit. The process will probably be lengthier and, as noted, the terms may be less appealing, but often credit can still be obtained.

Your Finances

- Credit and finances have improved. If your credit score has improved since your last mortgage application, you may be able to reduce the interest rates on your loan by refinancing. You can also save by refinancing if other financial indicators such as your debt, income and savings have improved.

- Credit and finances are the same. If your credit score and financial situation have not changed since your first mortgage, you may or may not be able to save with a refinance. Look at recent interest rate changes and consider your reasons for refinancing before you apply.

- Credit and finances are worse. If you’ve missed payments, run up big credit card bills or otherwise stressed your credit, you may not qualify for a low enough interest rate for refinancing to make sense. Estimate what mortgage rates you could receive and consider your reasons for refinancing before you apply.

- Stripped equity. To get the best rates, you’ll need to keep your borrowing on your refinancing loan to less than 80% of the value of your home. Refinancing might not make sense if you’ve already borrowed 90% or more of your home’s value in mortgages and home equity loans.

What Lenders Want

When deciding whether or not to grant a loan, creditors look for an ability to repay debt and a willingness to do so. When considering these factors they examine the three Cs of credit: capacity, character and collateral.

- Capacity. Can you repay the debt? Creditors ask for employment information: your occupation, how long you’ve worked, and how much you earn. They also want to know your expenses:

- How many dependents you have.

- Whether you pay alimony or child support.

- Amount of your other obligations.

The magic number that quantifies your capacity is your Debt-to-Income Ratio, or DTI. It is simply your total monthly payments divided by your gross monthly income.

- Character. Will you repay the debt? Creditors will look at your credit history to see how much you owe, how often you borrow, whether you pay bills on time, and whether you live within your means. They also look for signs of stability:

- How long you’ve lived at your present address.

- Whether you own or rent.

- Length of your present employment.

The important number here is your credit score. The higher, the better.

- Collateral. Is the lender fully protected if you fail to repay? Creditors want to know what you may have that could be used to back up or secure your loan, and what assets you have other than income for repaying the debt. In other words, what can they take from you if you default on the loan. The most important piece of collateral, of course, is the property you’re refinancing. The higher the loan amount relative to the appraised property value, the more nervous lenders get. This ratio, by the way, is called Loan-to-Value, or LTV.

Creditors use different combinations of these facts in reaching their decisions. Some set extremely high standards and other lenders simply do not make certain kinds of loans.

Some rely strictly on their own instinct and experience, while others use credit scores to predict whether you’re a good credit risk. They assign a certain number of points to each of the various characteristics that have proved to be reliable signs that a borrower will repay. Then, they rate you on this scale.

And so, different creditors may reach different conclusions based on the same set of facts. One may find you an acceptable risk, while another may deny you a loan.

Your Credit is Affected by Major Life Changes

- Marriage and divorce. While marriage can open financial opportunities for people who are now able to pool their resources most effectively, it also involves new responsibilities and issues for personal credit.

- Changing your name. If you change your name–at marriage or any other time-it is important that you make sure your creditors and the credit bureaus are notified of the change. Otherwise, you might lose your credit history.

- Keep credit in your own name. Women especially must take care to keep some credit in their own name-Judy Smith, rather than Mrs. John Smith, for example. Every year women who have never paid a bill late are denied credit because they have no credit history in their own names.

- Joint accounts mean joint responsibility. This is true even if a divorce decree includes provisions about one of the parties paying the bills. As far as a creditor is concerned, you are both responsible for the bills, even if only one of you ran up the charges. Arrangements must be made with the creditor, either through changing the account or closing it entirely and opening a new one, if one of you is to be released from liability for the debt.

- Purchasing a home. Buying a home makes significant demands on personal credit. It requires a solid credit rating, and once it takes place it can dramatically change some credit dynamics. On the one hand, homeowners build equity-an asset that contributes to their net worth-with each mortgage payment. They also establish another level of credit history and stability by making their mortgage payments on time. On the other hand, a mortgage is a large loan, and may impact things like your debt-to-income ratio in the first years of the loan.

- Having children. Beginning a family is another life change that puts demands on your credit. Many parents find that their credit card bills soar as they equip their homes and lifestyles to welcome and accommodate their children. But it’s especially important to take good care of your credit when you take on the added responsibility of children, using it wisely and managing it well. That way you know your credit will be available when you need it-like 18 years from now when those tiny infants head off for college.

- The death of a spouse. If you have a joint account with your spouse, by law a creditor cannot automatically close the account or change the terms because of the death of your spouse. More than likely, the creditor may ask you to update your application or reapply in your own name. The creditor will then decide whether to continue to extend you credit or change your credit limits. While your application is being reviewed, the creditor must let you use the account without new restrictions.

How Lenders Determine How Much Mortgage You Qualify For

- Lenders use two simple ratios to determine how much money you can borrow to refinance your home.

- Step 1: Write down your total gross pay per month, before deductions for taxes, insurance, etc.

- Step 2: Multiply the number in Step 1 times .28 (28%). This is the amount most lenders will use as the guideline for what your total housing costs (principal, interest, property taxes, and homeowners insurance, or PITI) should be. Some lenders may use a much higher percentage (up to 35%, but most people cannot realistically pay this much towards housing, and Ratio #2 often makes this a moot point).Example: The combined income for you and your spouse is $70,000, or $5,833 per month. ( $5,833 x 28% = $1,633.) Your total PITI should not exceed this amount.

- Debt to income.

- Step 1: Write down all of your monthly debt payments that extend for more than 11 months into the future, such as car loans, furniture or other installment loans, credit card payments, student loans, etc.

- Step 2: Multiply the number in Step 1 times .35 (35%). Your total monthly debt, including what you expect to pay in PITI, should not exceed this number.Example: You and your spouse have credit card payments of $200 per month, car payments of $183 and 350, student loan payments of $100 and $75, payments of $100 per month for furniture you purchased on a revolving credit account and will pay off over a two-year period, for a total monthly debt payment of $1,008.

Multiply your total monthly income of $5,833 per month times .35 (35%). Your total monthly debt, including PITI, should not exceed $2,041. Subtract your monthly debt payments of $1,008 from $2,041. This leaves you $1,033 a month for PITI.

Two Tips:

- If you are considering going into business for yourself or starting a new company, don’t! It is best to wait until your loan has gone through before making such a move.

- Making a major purchase at this particular time is not a good idea because it increases one’s debt to income ratio. If, for example, you were to add a $300 monthly payment on top of your current bills, you will now qualify for a mortgage payment that is $300 less. Any unnecessary major purchase should be made after your loan has been approved to determine what additional expenses you can take on.

Concerns When Tapping Equity and Consolidating Debt

Mortgage refinancing can be a slippery slope to never-ending debt. It’s important to keep this in mind when considering refinancing for the purpose of tapping into home equity or consolidating debt.

Homeowners often access the equity in their homes to cover big expenses, such as the costs of home remodeling or a child’s college education. These homeowners may justify such refinancing by pointing out that remodeling adds value to the home or that the interest rate on the mortgage loan is less than the rate on money borrowed from another source. Another justification is that the interest on mortgages is tax deductible. While these arguments may be true, increasing the number of years that you owe on your mortgage is rarely a smart financial decision, nor is spending a dollar on interest to get a $0.30 tax deduction.

Many homeowners refinance in order to consolidate their debt. Taking out extra cash during a refinancing to pay off credit-card debt is a popular tactic these days-and a huge potential mistake. You’ve turned what should be short-term debt into long-term debt, which can cost you more in the long run despite the tax advantages from being able to write off the interest. If you transfer $15,000 in credit cards to a new 30-year first mortgage, your monthly payments will be lower but it’s costing you more to pay off the revolving credit debt because of the lengthy term of the loan.

If you can swing it, you’re better off taking 10 years to pay off the charge cards because it will save you 20 years’ worth of additional interest.

Unfortunately, refinancing does not bring with it an automatic dose of financial prudence. In reality, a large percentage of people who once generated high-interest debt on credit cards, cars and other purchases will simply do it again after the mortgage refinancing gives them the available credit to do so. This creates an instant quadruple loss composed of wasted fees on the refinancing, lost equity in the house, additional years of increased interest payments on the new mortgage and the return of high-interest debt once the credit cards are maxed out again-the possible result is an endless perpetuation of the cycle of debt.

People who take out money to pay off credit cards and have no intention of changing their credit card behavior are at the top of the list of people who should not refinance.

When already in financial trouble, secured loans greatly increase the risk that you may lose your home. Alternatives should be considered such as reducing current expenses and increasing current income.