What to do to Refinance Auto Loan with Bad Credit? All of us plan to buy the dream car someday, but the budget always gets in between. Most of us try to opt for those tempting auto loans that are so much advertised but eventually some of us are unfortunate enough and we cannot pay it back.

This not only results in the loan being foreclosed and our beloved car taken away, but also results in bad credit rate. However, all is not lost since it is possible to refinance auto loan with bad credit. One simply has to know how to deal with banks and then work with a finance manager if necessary.

Table of contents

- WHAT ARE THE REASONS TO REFINANCE A CAR LOAN?

- WHAT TO DO TO REFINANCE AUTO LOAN WITH BAD CREDIT?

- ADVANTAGES OF CHOOSING A REFINANCE AUTO LOAN

- HOW TO AVOID REFINANCE AUTO LOAN SCAMS

- FINDING THE AUTO REFINANCE FIRM

- REFINANCE AUTO LOAN AFTER BANKRUPTCY

- HOW TO GET GUARANTEED AUTO LOANS FOR MILITARY

- BEST FOUR CONSIDERATIONS ON REFINANCE AUTO LOAN CALCULATOR

- CAN I REFINANCE A BALOON CAR LOAN?

What are the Reasons to Refinance a Car Loan?

All people have plans for the future, and to be able to secure it we must save money. Regardless of whether you’re saving for a new house or your child’s schooling, we have to take measures to do this. Lowering your overall expenses is among the least difficult and most reachable means to undergo to save a few bucks every day. Since most of the people have probably taken a loan for a car, a refinance auto loan is one way of reducing your expenses.

People may well have different motives as to why they require a refinance auto loan. Some could possibly be unable to pay ahead of the due date, while others might want to save money with lenders who provide low interest rates.

If you find it difficult to make your monthly payments, you’re in need of lenders that can offer lower interest rates or those that could extend the deadline for repayment. As your car would be one of the biggest payments each month, an easy solution for the problem will be trying to get a refinance auto loan. Your car loan may be due to the fact that you’ve picked the type for people with bad credit. At this stage, your credit standing would’ve improved after making a few on-time payments. This is actually the part where you could negotiate with your creditors on the setup of your payment method.

Possessing a better credit score, you have higher chances of getting approved for the revision of your contract. Start locating lenders that offer lower rates compared to the one you previously had. This is rather easy now as everything you need is within a few simple clicks. Search the internet for lenders and read carefully on their stipulations. Review the benefits you’ll get from possible choices of creditors.

Always remember that the interest rates may well rise and drop according to the market conditions as well as your recent credit ranking. Try to time your transaction well along these factors so you can get the most effective deals in renewed auto loan.

If you’re only bargaining for a new auto loan to spend less, you should study the market conditions. Whatever your purpose is, you should be cautious with the people you’re making transactions with. Confirm they are legal and that they aren’t a part of a fraudulent firm. You can do this easily as well through the Internet. Just do a thorough study on these credit companies and look for evaluations from past clients. Check the accreditation of their business and try to look for issues clients may have had with them in the past.

At times like this where so many people are just trying to survive financially, it usually is better to make sure everything is working on a legal scale. Before you even begin suspecting a company, make it to a point that you never give any private information to them. If you fall for the traps of these people, you could wind up losing more money than you intended to save.

Opt for a preowned auto loan?

Looking for a previously owned auto loan is much easier after you do it right online. There are many online lenders in which are in a position to give free quotes on their loans. Once you’ve collected several quotes from various direct lending companies online, do a comparison for top level terms and rates which would sell your home. Make use of an auto loan calculator, that is definitely found in many online lender websites, with an idea whether you possibly can really get yourself a car and watch the amount of you will definitely spend month after month to repay the financing. Since every home loan company offers different payments and annual percentage rates, auto loan calculators will make useful.

What to do to Refinance Auto Loan with Bad Credit?

What to do to Refinance Auto Loan with Bad Credit?

What to do to Refinance Auto Loan with Bad Credit?

What to do to Refinance Auto Loan with Bad Credit?Good news is, most loan companies understand that car loan is different from other loans and is more open to bearing with the debtor. In any other scenario, having a bad credit would mean that further loan applications for any kind of loan would mean rejection from all quarters. However, in case of auto loans, one can still get a loan, but with higher credit rate auto of interest than other customers and the loan company just might add some extra fees with it. It might seem like the loan company is taking advantage of the situation, but it is not. They are themselves in the subprime mess and as all of them are there to do business, they just have to charge this amount to mitigate their risks. Which means the monthly payment amount for the debtor is quite high combined with the higher interest and fees, but this is something that they just have to deal with.

in case of auto loans, one can still get a loan, but with higher rates of interest than other customers…

The debtors might think that well, if they had so much money to spare, then they would not have had bad credit in the first place. But there is still hope for them. Before banks think to refinance auto loan with bad credit, the debtor must at least make sure that the borrower has a good loan payment history on a fairly large trade line, which simply means that the financer will look at you as if you have a very good history of making long term payments, and you entered a bad credit phase simply due to some temporary financial crunches.

Moreover, since cars and automobiles will be looked upon as assets, it will seem like one of the most important assets were used to build the credit history back. In the long run, the debtor will eventually end up saving some money each month as the credit history starts improving and it keeps on adding to the payments loan history.

So the bottom line is that when the car was purchased, the buyer might not have been in a good position and perhaps did not even receive favorable terms upfront because of the bad credit history. But now that the financers see that the debtor has been making steady payments, they are more open about it. Moreover, this is something that the debtor himself has to believe in, that bad credit was just a temporary phase and would have to put forward his argument likewise. However, it is always better to be sure of one’s financial situation before opting to refinance auto loan with bad credit.

Make sure and only sign the papers if you are absolutely positive that you will be able to pay the higher rates of interests and fees this time. If not, than failure to pay your loan after you have refinanced will reflect on your credit history worse than ever before and you might never be able to get acceptable interest rates auto loan again in future. Also, have a look at our new article 5 Tips How to Get Auto Loan with Bad Credit.

How do I refinance my car?

You can find many choices for you to refinance your car. The best among your choices would be to get hold of your current lender. Ask them whether they can provide you with a better interest rate on your current loan. If they are unable to, maybe you could find out if they can simply extend the payoff period of your loan. This method could help save expenses associated with lien transfer fees and could spare you the need for finding a new lender.

Searching on the internet can help you for those who choose to seek out another lender that can offer you the best rates and terms on your new loan. This would allow you to compare lenders with regards to the rates they have and terms they’ve got. After making a wise evaluation of your options, select your lender and apply for the refinance loan with them. Normally, they’ll have to check your credit score. If you qualify for the refinance, they’ll pay off your present loan and your title is going to be transferred to them.

Refinance is not going to only give lower interest rates and reduced monthly payments, but also provides stress relief. There’s nothing more relieving for a refinancer like you than seeing monthly bills drop and knowing that you pay less interest.

Advantages of Choosing a Refinance Auto Loan

The refinance auto loan is a service offered by money lenders for consumers wishing to lower the amount of money they are paying on a car loan. Companies usually offer potential borrowers lower rates of interest on a refinance auto loan than on a new car loan. If car owners are experiencing difficulties in repaying their car loan, it can be a wise decision to refinance the car loan. It doesn’t matter whether the car is new or old, but as vehicles lose value quickly, the longer you wait, the less chance you have of securing a keen, low rate of interest.

The refinance auto loan allows customers to pay off the loan on a monthly basis to money lenders. Depending on the lending firm, it’s possible for borrowers to pay installments on a quarterly, bi-annual or yearly basis. If you have some capital, it can also be possible for you to give it to the money lender as a lump sum. This could potentially lower the amount of interest you are paying, as well as decreasing the amount of time you are contractually bound to pay back the firm.

Information and advice on auto refinance loans and debt management are available on the internet. Consumer-based web forums are a great place to research money lending companies, as reviews and impartial reports are provided. On these websites, the section on auto refinancing allows the user to view graphs and feedback as to how many people have been satisfied with the money lenders’ services and how the refinance auto loan has worked out for them.

Many loans companies now have websites, with comprehensive information available on the services they offer and the criteria a potential borrower has to meet in order for the loan request to be accepted. The internet is also a good place to look for more information, as well as for applying online.

How to Avoid Refinance Auto Loan Scams

The concept behind car refinancing scams is quite simple: Lenders will try practically everything to trap an unsuspecting new customer into a loan with absurd interest rates. This is the dilemma many car loan borrowers are now facing. Not knowing how to pay off their previous loans, they seek out new lenders with high hopes to ease up the burden through refinancing. Due to their lack of knowledge about auto scams, however, they just end feeling used and abused.

There are three kinds of auto refinance loan scammers:

- hidden-fees scammer

- bad credit score scammer

- greedy scammer

The common denominator in this equation is the target, which is a naive, gullible, and unsuspecting new customer. The modus operandi of the hidden-fees scammers is fairly common sense. They attract people with impossibly low interest rates. To avoid them, you need to very carefully assess the offer. If the deal seems too good to be true, then it most probably it is. You will of course start to notice once the extra fees start piling up. These could be anything, such as; transaction fees, FICO fees (there’s no such thing), paper fees, appointment fees and so on. Remember the only fees concerned with car loan refinance are your standard lien transfer fees ($5 to $10) and the state re-registration fees ($10 to $75). Once you see anything other than those two, just leave.

To avoid the credit score scammer, be sure that you know your own credit score. Their modus is simply faking a bad credit score in order to trap a customer into a refinance auto loan with high interest rates. If you have your real credit slip with you, you have nothing to fear from these types of scammers. “Refinance my car” is your new choice.

The last one, however, takes some effort and patience to avoid. Honestly, you can’t always avoid them if you have a bad credit score. Increasing the interest rates provides a security blanket for the investors, and it is their only way to protect themselves. Unfortunately, a lot of lenders try to abuse this power to force new borrowers into unfair interests. To steer clear from this type of scam, always consider all of your options before signing up the papers.

Finding The Auto Refinance Firm

First and foremost, your credit history should be in good shape. It’s a good idea for you to get a copy of your credit report, because if you are in a good financial position, you could possibly be eligible for a low interest auto refinance loan. So to get the good refinance auto loan, make sure that you research the industry well and compare the different interest rates from the many lenders out there. Once you have read some customer reviews and company profile, you should be ready to approach one of these firms. Make sure that you read the application print in full detail before you take the decision to take a loan. If you really are considering taking the auto refinancing loan, remember to calculate how beneficial the switch of loan provider will be for you in the long term. Most of the time, it’s possible for borrowers to save some cash by taking out an auto refinance loan.

You can also take out such a loan for bill consolidation, and if you are considering taking out any loan, not just refinancing. This lumps all of your debts into one lump sum, allowing you to pay off one creditor at a potentially lower interest rate, rather than several loan providers at various rates of interest. You should also talk to a financial expert when looking for the right lender, which is usually deciphered by how many benefits a potential borrower may garner from the financial agreement. Online there are many good deals available, as money lenders vie for business.

In any case, if you get the loan for your vehicle at a high rate of interest you might opt for an auto refinance plan, when the interest rates are lower. Before applying for one of these loans, there are certain points of consideration which you should keep in mind when you are planning to take such action. So to get the good refinance auto loan, make sure that you research the industry well and compare the different interest rates from the many lenders out there. You can also take out such a loan for bill consolidation, and if you are considering taking out any loan, not just refinancing.

Refinance Auto Loan After Bankruptcy

You have a got a good job and are doing well currently. You have managed to get in to a stable financial position now. After moving towards better life, you wish to buy a car, but your past credit history would prove to be an obstacle in your finance for this new car.

Although you might have filed for bankruptcy due to non-payment of loans, you still have a doubt will you get a loan now. Will you be able to finance your car? What if I say YES? Yes, you can still try getting auto loans. Even after being failed in the past you can apply for credit after bankruptcy. You need to resort to certain credit repair measures and get your car financed.

After being bankrupt, you can get a finance for your car. However, you need to abide by certain rules and regulations. The following paragraphs will help you know how to get a finance after for a car after going bankrupt.

Bankruptcy filing is a very big decision and is very difficult for one to decide. It makes a person surrender all his/her assets and it always shows up in the individuals financial reports. It leads to bad scores and make sit difficult for one to procure any finances and if one gets loans it is difficult for them to get these loans at good interest rates. Your loan will usually be charged with high interest rates as compared to similar loans of equal amount to others.

Getting auto loan after going through bankruptcy is more easier then getting a new credit card. The car will be used by the lenders as a collateral. Collateral surety means that if you fail to pay the installments the lenders will confiscate your car.

Having gone through the bankruptcy phase, you can get finance for your car and qualifying only for ‘bad credit car loans’. The sub-prime lenders will lend loans under this category but at a higher rate of interest. They do not go through your financial history to lend you this new loan.

However applying for this new loan will need a proper analysis of your financial earnings by you. You need to understand how much you earn and how do you divide this income. You must ensure that you pay all your installments on time. Failing to pay installments will worsen your score and will get your car confiscated.

Procuring this loan will also help you improve your score and credit report. It is one of the ways of credit repair. Procuring auto credit after bankruptcy will also help you improve your overall credit score.

How to Get Guaranteed Auto Loans For Military

Military personnel have proven job stability which is important when it comes to approving loans. Here’s some really great news for all the men and women that are currently on active duty in the armed forces of the United States. They can now obtain guaranteed auto loans for military personnel to purchase any new or used vehicle that they are looking at buying. Military deployment can rapidly use up your finances and slow expenditure caused by shifting away from home can hurt your credit. There are even options:

- To refinance current military auto loans for lower rates or,

- Longer repayments programs and as a result, lower monthly payments.

These loans have many benefits when compared to regular auto loans. Let’s take a further look at these benefits and the requirements for approval of military auto loans. Military car loans tend to have considerably better terms than other auto loans. For instance and this is the most important point, you can obtain lower interest rates! That’s right lower interest rates when compared to the same person in civilian life.

It is not uncommon to hear that this is due to the fact that lenders subsidize these military auto loans themselves. However, since military personnel are more reliable in terms of income and continuity in the job, the risk for the financial lender is lower and as a result it is easier to offer lower interest rates and still obtain profit. It’s really a matter of believing that working with military personnel, all other things being equal, is a better than working with the same profile applicant in civilian life. Besides lower interest rates, military auto loans also feature several other benefits which make the very attractive.

These Include:

- More flexible repayment programs which imply lower monthly payments if the borrower wants them.

- More flexibility in the terms of the loan amount you can obtain. These translate to having more years to pay back the loan if this helps.

- Military personnel can get higher loan amounts on military auto loans than on regular vehicle loans. That’s right! Higher loan amounts!

Military personnel can obtain bad credit auto loans for military personnel with very flexible requirements for approval. There are however, some additional requirements that are not very hard to meet and have mostly to do with the particularities of servicing in the forces. Most lenders offer online military car loan applications but there is also the possibility of processing everything through regular mail. You should keep in mind that even though these military car loans are easier to qualify for, your credit report will still be pulled and analyzed. However, a knowing something is a good benefit as opposed to regular vehicle loans is:

- Military car loans do not require a fix residence or a steady job

- Even if you just enlisted in the forces you can still qualify for guaranteed auto loans for military

Not only do our military personnel have the opportunity of serving their country, they can, at the same time take advantage of a very favorable car loan and use it to buy their next car with very good financing. Many auto finance companies offer guaranteed auto loans for military members of our armed forces, past and present. We work with nationwide dealers to find best auto loans for military personnel because we do not believe that helping your country should option out from purchasing the new or used vehicles for you and family.

Best Four Considerations On Refinance Auto Loan Calculator

When you are planning to buy a car, in case you have a tool which gives estimates on the rates of interest, your chances of receiving the best rates becomes easier. You’re certainly more likely to achieve in getting a loan when you have this type of help. Once you could make your month to month installments often for any period of time you are able to sign up for automobile re-financing.

If that’s the case you possibly can make usage of a re-finance auto loan calculator to ascertain if you can have more affordable rates of interest. Understanding that, and also to provide consumers chance, allow me to share the very best four methods for utilizing refinance auto loan calculator:

- Refinance auto loan calculator is really a beneficial tool. It drastically adds to the state of one’s financial situation. What it really does is it assists you to make informed actions. This is very vital because you will realize how much money you are likely to preserve with a high percentage of precision. Not using this nicely or neglecting it might result in monetary instability. For instance, if it is not the right time for you to re-finance due to your bad credit, you may end up having greater problems.

- The calculator provides input areas where you need to enter all your present particulars. This can be appropriate because depending on the details it will give back the estimations. Essential details you need to type in are your present vehicle loan particulars, starting and ending dates, number of pending installments, regular monthly rates of interest, pending loan balance. It’s a good plan to possess all the documentation at hand before you begin using the calculator.

- Search on the internet for the re-finance auto loan calculators. This is usually a critical aspect simply because several vehicle loan companies have websites these days. Checkout if they give a refinance calculator. Almost all of the sites offer one for free. This can be a very quick as well as simple method. By working with this properly it is possible to assess if car refinancing is a good choice for you or not at present.

- Analyze meticulously whether or not re-financing is worth right now? This is yet another vital aspect to think about. If you had a low credit score when you’ve received your past loan, you may have faced substantial interest rates. Now say by making regular month to month installments at least for the past six months you got your credit standing enhanced. In cases like this, you can use a re-finance auto loan calculator and make a decision whether it is best if you apply for auto refinancing and thereby get more affordable rates of interest.

If you comply with these 4 strategies for refinance auto loan calculator, chances are that you may succeed at having more affordable interest rates speedily. Other people have succeeded with these four tricks for re-finance auto loan calculator and hence you can too!

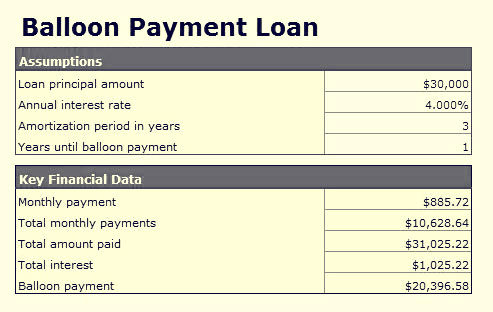

Can I Refinance a Baloon Car Loan?

A balloon loan is a good option if you need to keep your monthly payments low and know you’ll have the money to pay it off towards the end of the term. Additionally, balloon loans are an option for those people who absolutely need a new car but have no money for a down payment.

Plan in Advance

It’s important to plan for your balloon payment in advance. Save monthly, or invest with this in mind. You should also know that refinancing a balloon loan can be difficult. It may be possible to extend the length of your balloon loan at the end of the term, but that isn’t guaranteed. And if you do refinance, you might end up stretching your original three-to-five year term to seven years, or even longer.

It’s important to plan for your balloon payment in advance. Save monthly, or invest with this in mind. You should also know that refinancing a balloon loan can be difficult. It may be possible to extend the length of your balloon loan at the end of the term, but that isn’t guaranteed. And if you do refinance, you might end up stretching your original three-to-five year term to seven years, or even longer.

Not having the money for your balloon payment at the end of the loan is really the worst-case scenario for the lender — and for you. If you miss your payment, cannot make arrangements, or cannot refinance, you may lose the car even after you’ve paid the interest for all those years.

If you have the option to buy the car back, you still have to come up with the principal to do so. Under a normal loan, if you lost your car towards the end of the term you could buy it back for far less than you could with a balloon loan.